Days Sales Outstanding (DSO) is just a fancy way of asking: "On average, how long does it take for me to get paid after I do the work?"

Think of it like a stopwatch. It starts the second you send an invoice and only stops when that payment actually lands in your bank account. A lower number here is almost always a win because it means cash is flowing into your business faster.

What Days Sales Outstanding Really Means for Your Business

Let's make this real. Imagine you run a landscaping company and just wrapped up a big project. You send the invoice. That time you spend waiting for the client to pay up? That's the DSO for that single sale.

Your business's overall DSO is simply the average of all those waiting periods across every customer for a set timeframe, like a month or a quarter. It's one of the most honest numbers you can look at to understand your company's financial health.

Why Does This Number Matter So Much?

Knowing your DSO is like having a clear window into your business's cash flow. It tells you exactly how well you're doing at collecting the money you've already earned. This isn't just some accounting term; it directly impacts your ability to operate day-to-day.

A healthy, low DSO helps you:

- Pay Your Bills on Time: You need cash coming in to cover your own expenses—supplies, software, rent, you name it.

- Meet Payroll: Your team counts on you. A steady stream of cash from customers makes payday a routine event, not a stressful scramble.

- Fund Growth: Eyeing a new piece of equipment or ready to hire another person? Faster collections give you the cash to jump on those opportunities.

In short, your DSO shows how quickly you turn a finished job into usable cash.

To give you a quick snapshot, here’s what each part of the DSO puzzle tells you about your business.

DSO At a Glance

| Component | What It Means for Your Business |

|---|---|

| Accounts Receivable | This is the total money your customers owe you. A high number here isn't a good thing; it's cash you've earned but can't use yet. |

| Total Credit Sales | This is all the sales you've made that you haven't been paid for upfront. It's the source of your accounts receivable. |

| Number of Days | The time period you're measuring (e.g., 30 for a month, 90 for a quarter). This gives context for your DSO calculation. |

This table helps break down the moving parts, but the real story is what the final DSO number says about your operations.

Key Takeaway: A high DSO means your cash is trapped in unpaid invoices, which can create a serious bottleneck. A low DSO means your collections process is working, keeping your business financially healthy.

For instance, a construction contractor with a DSO of 60 days waits, on average, two full months to get paid after finishing a job. That makes it incredibly tough to buy materials for the next project or pay subcontractors on time.

On the flip side, a marketing agency with a 25-day DSO has a much shorter wait. That gives them far more freedom and flexibility to run their business.

Understanding what DSO is, and why it matters, is the first step. Next, we'll break down the simple formula to calculate this number for your own business.

How to Calculate Your Days Sales Outstanding

Figuring out your Days Sales Outstanding isn’t as complicated as it sounds. You don’t need a finance degree—just a simple formula and a few key numbers from your business records. Let’s walk through it.

The formula looks like this:

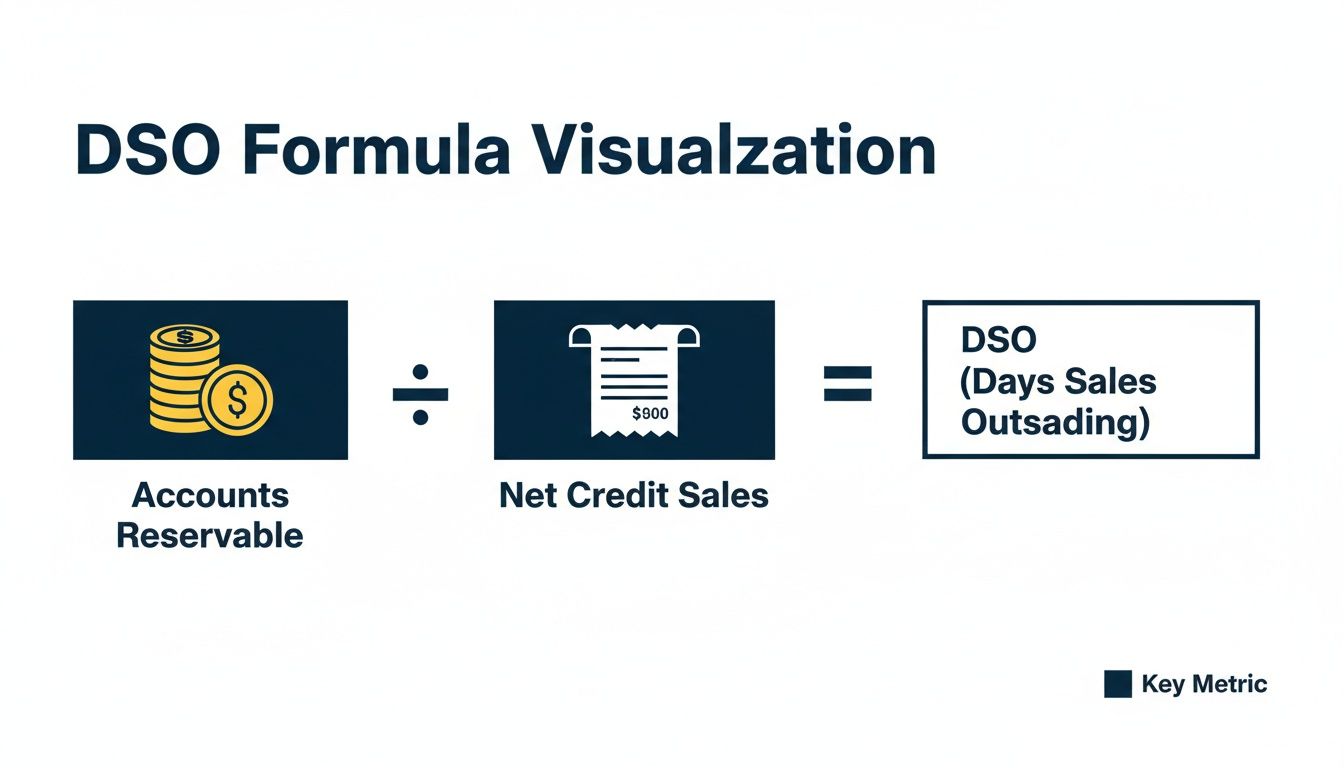

(Accounts Receivable / Net Credit Sales) x Number of Days in Period = DSO

That might look a little intimidating at first, but each piece is easy to understand once you know what you’re looking for.

Breaking Down the Formula

Before we plug in any numbers, let’s get clear on what each part of the formula means. Think of it like a recipe; you just need to know your ingredients.

- Accounts Receivable (AR): This is the total amount of money your customers owe you for products or services they’ve already received. It’s just the sum of all your unpaid invoices.

- Net Credit Sales: This is the total value of sales you made on credit during a specific period. It’s important to leave out cash sales here and subtract any returns.

- Number of Days in Period: This is just the number of days in the timeframe you’re measuring—30 for a month, 90 for a quarter, or 365 for a year.

You’ll find these numbers in your accounting software, whether you use QuickBooks, Xero, or something else. Your balance sheet will show your Accounts Receivable, and your income statement will have your Net Credit Sales. Keeping these records organized is a must for an accurate DSO calculation. Using professional tools like editable sample business receipt templates can help streamline your record-keeping.

A Real-World Calculation Example

Let's put the formula to work. Imagine you run a local contracting business and want to calculate your DSO for last month (we'll say it was a 30-day month).

You pull up your books and find:

- Total Accounts Receivable: $30,000

- Net Credit Sales for the month: $50,000

- Number of Days in the Period: 30

Now, we just plug those numbers into our formula:

($30,000 / $50,000) x 30 = DSO

First, do the division inside the parentheses:

$30,000 ÷ $50,000 = 0.6

Then, multiply by the number of days:

0.6 x 30 = 18

Your DSO is 18 days. This means that, on average, it takes your contracting business 18 days to get paid after sending an invoice. Honestly, that's a pretty healthy number!

This calculation gives you a powerful snapshot of your cash flow. Tracking it month-over-month helps you spot trends. Is your collection time getting longer or shorter?

For another perspective, consider BrightTech Solutions, a mid-sized software company. They calculated their Q1 DSO at about 64 days, which was a clear signal that they needed to tighten up their payment terms and get more serious with their collections process.

This simple calculation is the first step toward better cash management. For an even deeper dive into who owes you money and for how long, our guide on how to use an Accounts Receivable Aging Report Template is a great next step. Now, let’s figure out what a "good" DSO number actually looks like for your specific industry.

What a Good DSO Looks Like in Your Industry

So you’ve calculated your Days Sales Outstanding. Now for the million-dollar question—is your number good or bad?

The honest answer is: it depends. There’s no single “magic number” for DSO that works for every business.

What’s considered excellent for a construction company might be a total disaster for a retail store. The key is to compare your DSO to the average for your specific industry. This gives you real context and helps you see if you're a leader, average, or lagging behind the competition in getting paid.

Why Industry Averages Matter

Think of it like this: a baker expects to sell a loaf of bread the same day it's made. But a custom furniture maker knows it will take months to build and deliver a dining table, and their payment cycle will be much longer. Each industry has its own rhythm for payments, shaped by things like project length, customer expectations, and standard contract terms.

Comparing your business to others in your field is the only way to get a true sense of your performance. It helps you set realistic goals for improvement and understand what’s normal for your world.

This infographic breaks down the core components of the DSO formula we use to make these comparisons.

As you can see, the relationship between what you're owed and what you've sold on credit is the engine that determines how quickly you get paid.

Benchmarks Across Different Sectors

So, what do those typical numbers look like? Research shows a wide range of DSO averages across various industries. Some sectors get paid remarkably fast, while others have much longer, built-in waiting periods.

For example, a recent survey found that Technology & Professional Services averaged 34 days, while Distribution & Transportation was a bit longer at 41 days. This kind of industry-specific data is crucial for getting a clearer picture of where you stand.

Here’s a quick breakdown of average DSO numbers for a few common industries to give you a starting point.

Average DSO by Industry

Compare your DSO to the average for your industry to see where you stand.

| Industry | Average Days Sales Outstanding (DSO) |

|---|---|

| Finance & Real Estate | 11 days |

| Energy & Utilities | 19 days |

| Manufacturing & Construction | 21 days |

| Healthcare & Nonprofit | 22 days |

| Retail, Food & Entertainment | 26 days |

Seeing these numbers side-by-side makes it crystal clear how much payment cycles can vary. A real estate firm collecting payment in under two weeks is operating on a completely different timeline than a professional services firm that waits over a month.

The takeaway is simple: Don't just look at your own DSO in a vacuum. A high number isn't always a sign of trouble if it's normal for your industry. But if your competitors are collecting cash much faster, it’s a clear signal that there's room to improve your process.

Understanding your industry benchmark is a crucial first step. If you're consistently higher than the average, it's time to dig into why. This often points to issues with invoicing, follow-up, or even your initial payment terms.

Improving your DSO is directly related to how well you manage your entire accounts receivable process. Another key metric that works alongside DSO is the accounts receivable turnover ratio. You might be interested in our guide on what is accounts receivable turnover to see the full picture.

Now that you have the right context, let's look at what happens when your DSO creeps too high and the hidden risks it creates for your business.

The Hidden Dangers of a High DSO

A high DSO might just look like a number on a spreadsheet, but in reality, it’s a slow leak in your business’s fuel tank. It doesn't drain you all at once. Instead, it slowly siphons away the cash you need to operate and grow.

When you have to wait too long to get paid, it creates a constant, low-grade stress on your entire operation. It's the silent killer of cash flow, turning your hard-earned revenue into a number on a page instead of money in the bank.

The truth is, most businesses are in the same boat. A Kaplan Group survey of 100 finance leaders found that only a slim 14% keep their DSO under 30 days. A shocking 42% have to wait over 46 days to see their money, showing just how widespread this cash crunch really is. You can dig into their findings on why high DSO is a widespread challenge for businesses.

What Causes a High DSO in the First Place?

A high DSO rarely happens overnight. It’s usually the result of small, overlooked habits and broken processes that snowball over time. If you’ve noticed your DSO creeping up, it’s time to pop the hood and see what’s really going on.

Here are a few of the most common culprits I see:

- Confusing Invoices: Is your invoice a puzzle? If a customer can't instantly see what they’re paying for, the total due, and how to pay, they’ll almost always set it aside for "later."

- Inconsistent Follow-Up: Chasing payments only when you’re desperate for cash sends a clear message: paying on time isn’t a priority. A lack of a consistent follow-up process is practically an invitation for late payments.

- Overly Generous Payment Terms: Offering Net 60 or Net 90 terms might feel like a good way to win a client, but it guarantees you’ll be waiting months for your cash. Long payment windows can put a serious strain on your finances.

- Billing Errors: An invoice with the wrong amount, an incorrect PO number, or sent to the wrong person brings the payment process to a dead stop. The customer's clock stops ticking while you scramble to fix the mistake.

These might seem like minor operational hiccups, but each one directly inflates your DSO. You're effectively letting your customers use your business as an interest-free line of credit.

The bottom line is this: A high DSO is a symptom of a problem in your collections process. Finding the root cause is the first step toward plugging the cash flow drain.

The Real-World Risks of Slow Collections

When your DSO stays high, the consequences ripple far beyond simple inconvenience. It kicks off a chain reaction of financial problems that can stall your growth and even threaten your company's survival.

Let's break down the tangible risks you face when payments trickle in too slowly.

1. Cash Flow Strangulation

This is the most immediate and dangerous threat. Without a steady stream of cash, you can’t run your business. It's that simple.

You might find yourself struggling to:

- Pay your suppliers on time, which can wreck your business relationships and credit score.

- Meet payroll without anxiety, creating uncertainty for your team.

- Cover basic operating expenses, like rent, utilities, or software subscriptions.

This constant cash crunch forces you into a reactive mode, making decisions based on what you can afford today instead of what’s best for the business long-term.

2. Missed Growth Opportunities

Growth needs fuel, and in business, that fuel is cash. A high DSO keeps your money locked up in your customers’ bank accounts instead of yours.

This means you might have to pass on game-changing opportunities, such as:

- Hiring a key employee who could help you scale.

- Investing in new equipment that would boost efficiency.

- Launching a marketing campaign to land more clients.

While you're waiting to get paid, you're stuck in a holding pattern. Meanwhile, your competitors who get paid faster are lapping you.

3. Increased Risk of Bad Debt

The longer an invoice goes unpaid, the less likely it is you'll ever see that money. An invoice that's 90 days past due has a frighteningly high chance of becoming bad debt—money you eventually have to write off as a complete loss.

A high DSO means more of your invoices are sitting in that high-risk zone, which directly eats away at your profitability.

Now that we understand the dangers, the next step is to build a plan to fix them.

Actionable Strategies to Lower Your DSO

Knowing the dangers of a high DSO is one thing; actually fixing it is another. The good news is that you don't need a complicated, expensive plan to start getting paid faster. Small, consistent changes to your daily operations can make a huge difference.

Feeling stuck with slow payments doesn't have to be your new normal. Let’s walk through some practical, easy-to-implement strategies you can put into place today. Think of these as tweaks to your process, policies, and technology that directly boost your bank account.

Sharpen Your Invoicing Process

Your invoicing process is the starting line for getting paid. A sloppy start almost guarantees a slow finish. The goal is to make your invoices so clear and easy to handle that paying them becomes the path of least resistance for your customers.

Start by sending invoices the moment a job is done or a product is delivered. Don't wait until the end of the month. The sooner the invoice is in their hands, the sooner it enters their payment system.

Here are a few more simple process fixes:

- Keep Invoices Simple: Make sure the invoice clearly states who it's from, what it's for, the total amount due, and the due date. Avoid clutter and confusing line items.

- Confirm the Recipient: Before you even send it, confirm you have the correct contact person and email address for the accounts payable department. Sending it to the wrong person is a guaranteed delay.

- Offer Multiple Payment Options: Make it easy for people to pay you. Accept credit cards, ACH transfers, and online payments. The fewer hoops a customer has to jump through, the faster you get your money.

Key Insight: Your invoice isn't just a request for money; it's a communication tool. A clear, professional, and prompt invoice tells your client that you are organized and expect to be paid on time.

For any business, especially those in specialized fields, clear communication is critical. Implementing effective medical billing AR follow-up is a direct way to reduce outstanding payment times and, consequently, your DSO in the healthcare sector. The same principle of clear, persistent follow-up applies to every industry.

Set Clear and Firm Payment Policies

Your payment policies set the rules of the game. If your rules are vague or you don't enforce them, you can't be surprised when customers pay late. It's time to be upfront and firm about your expectations from the very beginning.

This starts before you even do the work. Your payment terms should be clearly stated in your contracts, proposals, and on every single invoice. Terms like "Net 30" should be impossible to miss.

Consider these policy adjustments:

- Tighten Payment Terms: Are you offering Net 60 or Net 90 terms? For most small businesses, that's far too long. Try moving to Net 30 or even Net 15.

- Offer Early Payment Discounts: A small discount like "2% 10 Net 30" (a 2% discount if paid in 10 days) can motivate customers to pay you much faster. It's often cheaper than chasing a late payment.

- Implement Late Payment Fees: Clearly state that a late fee will be applied to overdue invoices. Even a small penalty can be a powerful motivator for customers to pay on time.

Even a slight increase in DSO can have a big impact. By Dec. 2024, C.H. Robinson Worldwide's DSO climbed to 54.67 from 52.13 in Dec. 2023—a 4.9% rise that signaled slips in their collection process. This shows why having firm policies is so crucial.

Use Technology to Automate Your Collections

Manually tracking invoices and sending reminder emails is a time-consuming chore that’s easy to let slide. This is where technology becomes your best friend. Modern accounting software can automate much of this process for you, ensuring nothing slips through the cracks.

Set up automated payment reminders in your accounting system (like QuickBooks or Xero). You can schedule gentle reminders to go out a few days before the due date, on the due date, and at regular intervals after the due date. This consistency is key.

Automation helps in several ways:

- Saves You Time: Frees you up from tedious administrative work so you can focus on running your business.

- Ensures Consistency: Reminders go out on schedule every time, without fail.

- Removes Awkwardness: Automating the follow-up takes the personal emotion out of chasing payments. It’s just the system doing its job.

These strategies are all part of a larger system for financial health. Check out our guide on how to manage accounts receivable effectively for more tips on building a robust collections system.

How to Master Your DSO and Free Up Your Time

As a business owner, your job isn't to be a professional bill collector. Let's be honest, you didn't start a company to spend your days chasing down payments when you could be serving customers and growing your business. Mastering your Days Sales Outstanding is about getting that time back.

This is where all the pieces we've talked about come together. It’s about shifting from constantly worrying about cash flow to confidently managing it. The goal is to get your business to a place where your money works for you, not against you.

From Worrying to Winning

The key to getting a handle on your DSO is having clean, reliable books. When your financial records are a mess, you can't see problems coming until they’ve already hit. But when your books are accurate? You can build clear financial dashboards that give you an at-a-glance view of your cash flow health.

Imagine knowing exactly who owes you money, how long they've owed it, and what your cash position will look like next week. That’s the kind of clarity that lets you make smart decisions instead of just guessing. You can decide when to hire, when to invest in new equipment, and when to push for more sales—all based on real data.

This isn't just about managing a number. It's about building a system that puts you back in control, freeing you from the day-to-day stress of chasing cash so you can get back to leading your business.

Putting the right systems in place means you spend less time in the weeds and more time on what actually matters. This becomes even more critical as a business grows. Research from CFOs shows that while larger firms often see a higher DSO simply from having more customers, small businesses can beat this trend with responsive teams. These teams can handle everything from payroll to forecasting, turning financial data into real growth plans. You can read more about these survey insights to see just how much a proactive approach pays off.

Common Questions About DSO

We've walked through what Days Sales Outstanding is and how you can start wrangling it. But if you're like most business owners I talk to, you probably still have a few questions rolling around in your head. Let's tackle the ones that come up most often.

How Often Should I Calculate My DSO?

For most businesses, calculating your DSO every month hits the sweet spot. It’s frequent enough to spot trouble before it snowballs but not so often that you feel like you're just crunching numbers all day.

Now, if you’re in a business with a high volume of daily sales—think a busy contractor or a popular e-commerce store—you might want to peek at it weekly. The most important thing isn't the frequency, it's the consistency. Tracking it regularly is the only way to know if the changes you're making are actually helping you get paid faster.

Does a Lower DSO Mean My Business Is More Profitable?

Not directly, but a low DSO is a massive step in the right direction. Think of it like this: DSO measures the speed at which you collect cash, while profit is what’s left after you pay all your bills.

Getting your cash in the door faster (a low DSO) gives you the fuel you need to run the business without constantly feeling stressed. It means you can pay suppliers on time, avoid leaning on expensive lines of credit, and jump on opportunities that lead to more profit. So while DSO is about cash flow velocity, improving it almost always strengthens your bottom line.

Key Takeaway: A low DSO gives your business the fuel it needs to operate efficiently and chase profitable opportunities. It’s a health metric that leads to better financial performance.

Can My DSO Be Too Low?

Believe it or not, yes. An extremely low DSO can be a red flag that your payment terms are actually too strict and might be hurting sales.

For example, if you demand payment upfront for every single service, your DSO could be near zero. Sounds great, right? But you could be chasing away perfectly good customers who just need a little flexibility. Meanwhile, your competitors offering standard 30-day terms might be scooping up that business.

The goal isn't to hit the lowest possible number at any cost. It's to find that sweet spot—a DSO that keeps cash flowing in steadily without making it a hassle for good customers to do business with you.

Feeling like you're spending more time chasing invoices than running your business? MyOfficeOps can help you put the systems in place to get paid faster and take control of your cash flow. We provide the bookkeeping, reporting, and expert advice you need to master your DSO and win back your time.

Ready to get a clear picture of your finances? Schedule a Discovery Call with us today!