Bookkeeping for law firms isn't just about tracking money. It's a special skill. Unlike regular business accounting, it has strict rules for handling client money held in trust. Getting this right isn't just a good idea—it’s a must for staying out of trouble and running a profitable firm.

Why Smart Bookkeeping Is a Must-Have for Law Firms

Let's be real, you went to law school to be a lawyer, not an accountant. But when you run a law firm, you're also running a business. Think of your bookkeeping as the heartbeat monitor for your practice. It’s the only way to know if you're making money, where it's going, and whether you're about to cross an ethical line.

The #1 rule in legal bookkeeping is simple and you can't ever break it: never mix your money with your client's money. This is the core of trust accounting, which is usually managed through an IOLTA (Interest on Lawyers' Trust Accounts). It’s like holding onto a friend's cash for them; you wouldn't use it to buy your own lunch, right? The idea is the same, but the consequences of getting it wrong are much, much worse.

The Foundation of a Healthy Practice

Good bookkeeping is more than a chore you do at tax time. It's a daily habit that gives you a clear financial picture, helping you make smarter decisions. When your books are clean, you can finally get straight answers to the big questions.

- Which practice areas are actually making money? Good records show you which services bring in the most cash, so you can stop guessing and focus your efforts where they count.

- Is our cash flow healthy? You’ll know if clients are paying on time and if you have enough money to cover payroll and rent without that knot in your stomach.

- Are we pricing our services right? By tracking what you earn against the time and costs for each case, you can see if your billing rates are really helping your firm grow.

Clean books give you more than just peace of mind with the rules; they give you the clarity you need to turn your law practice into a predictable, profitable business. Without them, you're flying blind.

More Than Just Numbers

Beyond the money side, solid bookkeeping builds trust with everyone—clients, banks, and especially regulators. Messy records don't just look bad; they are a huge red flag during an audit.

Of course, this whole system needs a solid tech backbone. To protect sensitive client data, you need the right IT solutions for law firms. This isn't just a good idea; it's essential for secure and effective bookkeeping.

In the end, proper bookkeeping for law firms means you follow the rules, understand where your money comes from, and sleep better at night. It's the foundation that lets you stop worrying about the numbers and focus on what you do best: winning for your clients.

Mastering Trust Accounting and Avoiding Common Pitfalls

If there's one part of law firm bookkeeping that keeps lawyers up at night, it's trust accounting. This isn't just a banking rule; holding a client's money is a serious duty. Get it right, and you build a rock-solid foundation of trust. Get it wrong, and you could face serious trouble, even losing your license.

The key to getting this right is a process called three-way reconciliation. It sounds complicated, but it's just like three friends checking their stories to make sure every single detail matches perfectly.

The Three Matching Stories

For your trust account to be perfect, you need three separate records to show the exact same total balance at the end of every month. No excuses.

- Your Trust Bank Statement: This is the official record from the bank showing every dollar that came in and went out. It's the source of truth.

- Your Internal Trust Ledger: This is your firm’s own running list of all transactions for the trust account as a whole. Think of it as your master checkbook register for the trust account.

- The Sum of All Individual Client Ledgers: This is where the details live. You must keep a separate, detailed record for each client, showing exactly how much of the money in the trust account belongs to them. When you add up the balances for every single client, that total must match the other two records.

If these three numbers don't match to the penny, it’s a big problem. It means a mistake was made somewhere—a transaction might be missing, or even worse, one client's money might have been used for another's case.

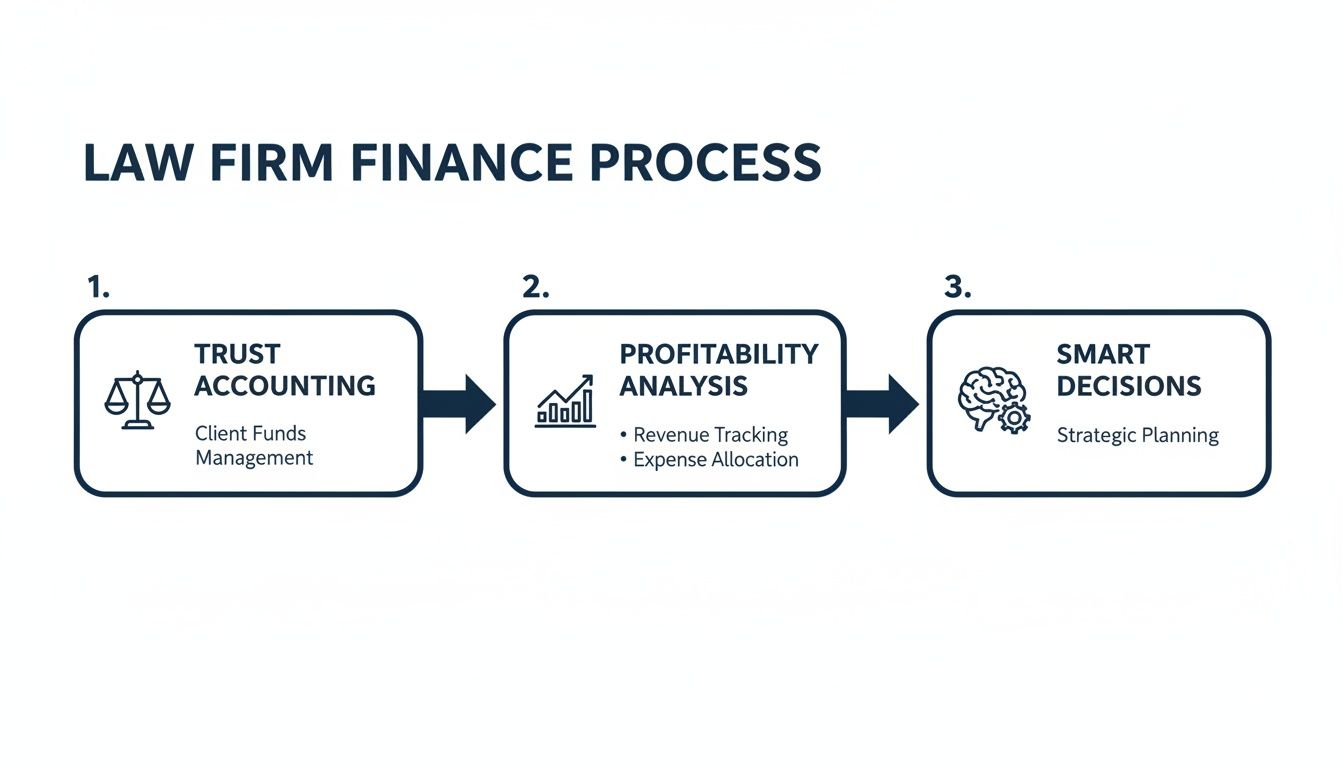

This visual shows how proper trust accounting is the first step toward understanding your firm's profitability and making smart financial decisions.

The process is clear: mastering trust rules is the foundation. Only then can you accurately measure your firm's financial health and guide its future with confidence.

Common Mistakes That Land Firms in Hot Water

Most problems don't happen because of bad intentions. They happen because of simple, preventable mistakes. But even a small error can be seen as a serious breach of your duty.

Here are the most common traps you have to avoid:

- Commingling Funds: This is the biggest sin of trust accounting. It happens the moment you mix your firm’s operating money with client trust funds. Even putting a small amount of firm money in the trust account to cover bank fees (unless your state bar specifically allows it) is a major violation.

- Paying Firm Expenses from Trust: Never, ever use the trust account to pay for office coffee, rent, or payroll. That money does not belong to you. It's like using your friend's savings account to pay your electric bill.

- Using One Client's Money for Another: This is a huge no-no. If you need to pay a filing fee for Client B but their retainer hasn't cleared yet, you cannot "borrow" from Client A's funds, even for five minutes. Each client's money is completely separate and can only be used for their specific case.

The rule is simple: the money in your trust account is not your money. You are just holding it for safekeeping until it's either earned and properly moved to your operating account or returned to the client.

Another common error is not keeping detailed records for each client. You must be able to show a complete history of every dollar for any specific client at a moment's notice.

For a deeper look, check out our guide on professional law firm accounting services to see how experts handle these exact challenges. By treating client funds with the discipline they deserve, you protect not only your clients but your license and your firm’s reputation.

How To Set Up Your Chart of Accounts

Think of your Chart of Accounts as the financial filing cabinet for your law firm. Every single dollar that comes in or goes out gets sorted into a specific folder, or "account." For a law firm, using a generic filing system from a standard accounting program just won't work.

That’s like trying to organize complex case files using a system designed for a pizza shop—it’s a recipe for chaos and bad information.

Your firm has unique financial activities that need their own dedicated folders. A generic setup just lumps everything together, making it impossible to see the real story behind your numbers. Proper bookkeeping for law firms starts with a custom Chart of Accounts. This isn't just for accountants; it's your financial roadmap. A well-organized chart tells you exactly where your money is coming from and where it's going, helping you make smarter business decisions.

Why a Generic Chart of Accounts Fails Law Firms

A standard Chart of Accounts might have one big folder labeled "Income." But what does that really tell you? Not much. For a law firm, knowing the type of income is critical.

Money from a big contingency fee case tells a very different story about your cash flow than money from a steady hourly client. Lumping them together hides important information. You need to know which practice areas bring in steady cash and which bring in those large, but less frequent, payouts.

The same problem happens with your expenses. You have to separate the costs directly tied to a client's case from your firm's general overhead.

- Advanced Client Costs: These are expenses you pay for a client, like court filing fees or hiring an expert witness. You expect to get this money back.

- Firm Operating Expenses: This is your overhead—think office rent, staff salaries, and software. These are the costs of keeping the lights on.

Mixing these two gives you a totally wrong idea of your firm's profitability. You might think you're spending a ton on office supplies when a huge chunk of that is actually client costs that will be paid back to you. For a deeper look, you might want to learn more about what is a chart of accounts and why its setup is so important.

A custom Chart of Accounts is the difference between looking at a blurry financial picture and seeing a crystal-clear image of your firm's health.

Key Accounts Your Law Firm Needs

Setting up your chart of accounts correctly from day one will save you a ton of headaches later. It makes sure your financial reports are accurate and, more importantly, useful. Here’s a simple look at the essential "folders" every law firm should have in its financial filing cabinet.

Sample Chart of Accounts for a Law Firm

This table shows a basic but essential setup that gives you the clarity you need to run your practice well.

| Account Category | Account Name | What It's For (Simple Explanation) |

|---|---|---|

| Assets | IOLTA/Trust Bank Account | The special bank account where you hold all client money. This is NOT your money. |

| Assets | Operating Bank Account | Your firm's main checking account for paying bills and receiving earned fees. |

| Liabilities | Client Trust Liability | This account matches your IOLTA bank account. It shows you how much you owe to your clients. |

| Income | Legal Fees – Hourly | All the money you earn from billing clients by the hour. |

| Income | Legal Fees – Contingency | The income you get from winning contingency cases. |

| Income | Legal Fees – Flat Fee | Money from services you provide for a single, fixed price. |

| Expenses | Advanced Client Costs | Money you spend for a client that you will bill them for later (e.g., expert witness fees). |

| Expenses | Payroll Expenses | Salaries and wages you pay to your staff and lawyers. |

| Expenses | Rent and Utilities | The cost of your office space, electricity, and internet. |

| Expenses | Malpractice Insurance | Your professional liability insurance payments. |

This setup immediately gives you clarity. By separating your income, you can instantly see which billing model is making you the most money. And by separating client costs from firm overhead, you get a true measure of your operating expenses, which makes budgeting much more accurate.

Streamlining Billing and Retainer Workflows

Getting paid for your hard work shouldn’t be the hardest part of running a law practice. For too many firms, though, messy billing is a constant source of frustration and lost money. Getting this process right doesn't just improve your cash flow; it shows clients that your firm is professional and organized.

It all comes down to one simple thing: tracking your time. Every six-minute block you forget to log is money you’ve just given away for free. Think of it like a coffee shop forgetting to charge for every tenth cup—those small amounts add up to a huge loss over a year. The good news is, modern tools can make this almost automatic.

Making Retainers Simple and Compliant

One of the biggest traps in bookkeeping for law firms is handling retainers correctly. If you only remember one thing, make it this: an upfront retainer is not your money yet.

I like to compare it to a security deposit on an apartment. The landlord holds the cash, but it still belongs to the renter until they move out and any damages are added up. A client's retainer works the same way. In accounting, it’s a liability—money you owe back to them until you’ve actually done the work to earn it.

A retainer is a promise of future payment held in trust. It only becomes your income after you have done the work, sent a detailed invoice, and properly moved the money from your trust account to your operating account.

This isn’t just an accounting rule; it’s the most important part of trust accounting. That money has to sit in your IOLTA account, completely separate from your firm’s day-to-day operating funds. As you do work each month, you send the client a detailed invoice. Only after that invoice is sent can you move the exact amount you earned from the trust account into your business account. This isn't a suggestion—it's a critical ethical rule.

Improving Your Invoicing and Collection Process

How you bill is just as important as what you bill. If your invoices are confusing, late, or a pain to pay, you're creating your own collection problems. It's no surprise that, on average, lawyers only collect 85% of what they bill. A huge chunk of that missing 15% comes from clunky, slow billing habits.

Your goal should be to make it super easy for your clients to understand their bill and pay you right away. This comes down to a few key actions:

- Send Itemized Invoices Promptly: Don't wait. Billing for work done in the first week of the month shouldn't wait until the 30th. Sending invoices quickly, while the value of your work is still fresh in the client’s mind, makes it much more likely you'll get paid without a follow-up.

- Make Invoices Easy to Read: Get rid of the dense blocks of legal language. Your invoice should clearly state the work done, who did it, how long it took, and the cost for each item. A clear invoice builds trust and cuts down on the questions that delay payment.

- Offer Simple Online Payment Options: In a world where you can buy groceries with your phone, forcing clients to mail a paper check is just adding hassle. A simple "Pay Now" button on your invoice that links to a secure online portal can slash your collection times.

I saw this work perfectly with a small family law practice. They were tearing their hair out over an average payment time of 45 days. They made one change: they stopped emailing PDF invoices and started using a system that sent professional, itemized bills with a direct link to pay by credit card.

The result? Their average time to get paid dropped to just 18 days. This simple switch didn't just fix their cash flow; it freed up their paralegal from chasing late payments, letting her focus on valuable, billable work instead.

Choosing the Right Bookkeeping Software

The right software can be a huge help in managing your firm's finances, but picking the best tools can feel like a lot. You don’t need to be a tech genius to make a smart choice. The key isn't finding one perfect program that does everything; it's about building a system where your tools work together as a team.

Think of it this way: your legal practice management software is where you handle cases, track your time, and create invoices. Your accounting software, like QuickBooks Online, is the firm's financial engine—it manages payroll, taxes, and the overall health of the business. They have to talk to each other.

Creating a Seamless Connection

When these two systems are connected, information flows automatically. This connection, or integration, is like building a bridge between two islands. Without that bridge, you'd have to manually load all the information onto a boat (that's you or your staff) and sail it back and forth every single day. It’s slow, boring, and things can easily get lost or mixed up.

A good integration builds that bridge for you. When you log billable hours in your practice management software, the information just shows up in your accounting software. This one step gets rid of hours of manual typing and drastically cuts down on the risk of human error.

The goal is to build a system where you only have to enter information once. When your tools talk to each other, you get more accuracy and free up valuable time that should be spent on law, not on spreadsheets.

What to Look for in Legal Software

Instead of just listing a bunch of software names, let’s focus on what really matters. Your firm needs a setup that handles the unique needs of legal bookkeeping, especially the tricky parts of trust accounting.

- Trust Accounting Features: Your software must have tools to manage your IOLTA account. It should let you easily track individual client ledgers and perform the three-way reconciliations we talked about earlier.

- Time Tracking and Billing: The system should make it incredibly simple for you and your staff to capture every billable minute. Look for features that allow for easy, itemized invoicing and online payment options.

- Strong Integration Capabilities: Make sure your chosen practice management tool connects smoothly with a major accounting platform like QuickBooks Online. This is a must-have for an efficient process.

Choosing the right platform is a big decision for your firm's efficiency. To help you sort through the options, a detailed comparison of leading legal software like Clio vs. MyCase can be a big help. It breaks down the features that matter most to small firms.

Ultimately, the best bookkeeping for law firms combines a specialized legal tool with a powerful, general accounting engine. For more ideas on general tools, you can explore our list of the best accounting software for small business to see what might fit your needs. By focusing on how these tools connect, you create a reliable system that supports your firm’s growth and lets you focus on your clients.

When to Outsource Your Firm's Bookkeeping

Sooner or later, every law firm owner hits a wall. You just can't do it all. The idea of outsourcing your firm's bookkeeping can feel like a big step, but it’s not just about hiring help; it's a smart move to get your time back and grow your practice.

Many lawyers think doing their own bookkeeping saves money. This ignores the hidden cost: your own time. What is one of your billable hours worth? Every minute you spend trying to fix a number or chase down an invoice is a minute you aren't spending on client work, preparing for a case, or finding new business. That hurts your bottom line.

Is It Time to Make the Switch?

The need to outsource isn't usually a single, big event. It’s more of a slow burn—a handful of small, ongoing frustrations that tell you it's time to bring in a pro. Ignoring these signs doesn't make them go away; it just leads to bigger headaches like compliance mistakes or missed chances to grow.

Here are a few signs that doing it yourself is holding you back:

- You're Always Behind: Is bookkeeping the one task that always gets pushed to nights and weekends? If so, your financial information is always old, making it useless for making good decisions.

- You Dread Tax Season: If the thought of tax prep makes you anxious, it’s a clear sign your records aren't clean and organized during the year. A good system makes tax time no big deal.

- Your Reports Are Gibberish: You print a Profit & Loss report, but you have no real idea what it's telling you about your firm's health. The numbers are there, but the story is lost.

- You've Made a Trust Accounting Mistake: This is the big one. Even a small error with a trust account is a serious ethical problem. If you find one mistake, there are probably others you haven't found yet.

Outsourcing isn't giving up. It's recognizing that your time is best spent practicing law, not fighting with spreadsheets. The cost of an expert is almost always less than the cost of your own lost billable hours and the stress of managing it all.

The Real-World Impact of Outsourcing

Let me tell you about a small firm I know. The founding partner was a great trial lawyer, but he was losing every Saturday morning to a fight with QuickBooks. He was stressed, his books were a mess, and he felt totally out of touch with the financial side of his own business.

He finally decided to outsource. The change was almost instant. He got his weekends back, which made him sharper and better prepared for his cases. But the biggest benefit was something he didn't expect: clarity.

His new bookkeeping team gave him simple, clear financial reports each month. For the first time, he could actually see which case types were making him the most money and which were just eating up time. With this knowledge, he shifted his firm's focus. The result? His profits jumped by 20% in the first year alone.

He didn't just buy a service; he invested in a system that helped him build a smarter, more profitable firm. That’s the real value of bringing in a professional.

Have More Questions? Let's Cover the Common Ones.

Even after you learn the basics, a few questions always seem to come up about bookkeeping for law firms. Let's go through the most common ones I hear with some simple, straight answers.

What Is the Biggest Bookkeeping Mistake a Law Firm Can Make?

The single most dangerous mistake is messing up the client trust account. This isn't just a simple typo; it’s a huge ethical violation that can get you disbarred. Seriously. It includes mixing firm funds with client money (commingling), borrowing from one client's funds to pay for another's, or just keeping sloppy records.

Imagine you're holding money for two different friends. You'd never use Friend A's money to cover something for Friend B, right? The same strict rule applies here. A very close second is not tracking all your time—that’s just leaving money on the table.

How Often Should I Actually Look at My Firm's Financial Reports?

You need to be looking at your Profit & Loss statement and your Balance Sheet every single month, at the very least. Think of it as your firm's monthly health check-up. These reports are the only way to know if you're actually making money and what your firm's overall financial situation looks like.

Looking at them regularly helps you spot problems early, like a sudden jump in expenses or clients taking longer to pay their bills. This lets you fix the small issues before they turn into the big, stressful problems that keep you up at night.

Can I Just Use a General Bookkeeper for My Law Firm?

Honestly, using a general bookkeeper is a huge risk. They might understand basic accounting, but they almost certainly don’t know the specific, strict rules for legal trust accounting. One small mistake with a trust account—something a general bookkeeper might not even see as a mistake—could put your law license on the line.

It's much safer to work with a bookkeeper or a service that specializes in the legal industry. They know the unique compliance rules inside and out, protecting you from potentially career-ending errors.

What's the Best Software Setup for a Law Firm?

The best setup usually involves two types of software that work together like a team.

- Legal Practice Management Software: This is your command center for the day-to-day work of being a lawyer. It handles things like case management, tracking your time, and sending out invoices. Think tools like Clio or MyCase.

- Accounting Software: This is for the business side of your firm—paying the bills, managing payroll, and getting a clear picture of your overall finances. QuickBooks Online is the big player here.

The most important part is that these two systems integrate, meaning they talk to each other and share data automatically. This connection saves tons of time on boring data entry and, more importantly, prevents the kinds of human errors that can get you into serious trouble.

Ready to stop worrying about your books and get back to focusing on your clients? The team at MyOfficeOps specializes in bookkeeping for law firms, providing the financial clarity and compliance peace of mind you need. Learn more at https://myofficeops.com.