You pull up your P&L, glance at the bank balance, and still can't answer the questions that matter.

Can you afford to hire? Is that new service line making money? Did your last marketing push help, or did it just make revenue look busy for a month? Most owners in West Chester, Philly, and the surrounding suburbs don't have a reporting problem. They have a decision problem.

That's where people start asking what is financial advisory services, and the usual answers fall flat. They talk about investments, retirement accounts, and generic money management. But if you own an operating business, you need something more practical. You need help turning numbers into moves.

Why Your Business Numbers Feel Stuck in the Past

A lot of owners are running the business by checking three things. Revenue, cash in the bank, and whether payroll clears on Friday.

That works for a while. Then the business gets bigger, expenses get messier, and timing starts to bite you. Revenue might look fine on paper while cash gets tight. You might land more work and still feel less stable than you did six months ago.

I see this all the time with service businesses. A firm gets monthly reports from QuickBooks or Xero, maybe even from a decent accountant, but the reports mainly tell them what already happened. They don't tell them what to do next.

The real frustration isn't bad data

The primary frustration is this kind of question loop:

- Hiring question. Can I bring on one more person without hurting cash flow?

- Pricing question. Are my rates too low, or do I just have a cost problem?

- Growth question. Should I push for more sales right now, or fix operations first?

- Owner pay question. Am I taking too much out of the business, or not enough?

Historical reports rarely answer those on their own. They're like a scoreboard after the game. Useful, yes. But they won't help you call the next play.

Financial advisory starts where basic reporting stops. It turns backward-looking numbers into forward-looking decisions.

That need is one reason the market keeps expanding. The global financial advisory services market was valued at USD 85.1 billion in 2022 and is projected to reach USD 146.8 billion by 2032, according to Global Market Insights on the financial advisory services market.

What changes when advisory enters the picture

Instead of just sending reports, a good advisor helps you ask:

- What's changing in gross margin?

- Which clients or jobs create cash strain?

- How much working capital do you really need?

- What happens if sales slow, or if you hire sooner than planned?

If your current reporting still feels like a history lesson, cleaner systems help. Even simple process improvements like financial reporting automation for small businesses can make your numbers more timely, which makes the advice more useful.

Thinking Like an Advisor Not Just an Accountant

A simple way to think about it is this.

Your accounting is the rearview mirror. Your financial advisory is the GPS.

You need both. If the mirror is missing, you can't see where you've been. If the GPS is missing, you may still be driving, but you're guessing at every turn.

What an advisor actually does

At its core, financial advisory is a decision-support function. The advisor takes your goals, your financial data, and outside knowledge about markets, debt, risk, and planning, then uses that information to improve decisions on assets, liabilities, and capital. That's the practical definition in Indeed's financial advisor job description guide.

For a business owner, that usually means things like:

- Choosing timing. Not just whether to hire, but when.

- Testing scenarios. What happens if payroll rises before collections improve?

- Spotting weak profit. Revenue can hide bad margins.

- Reducing avoidable risk. Debt, taxes, and poor cash timing hurt more than most owners expect.

Where owners get tripped up

Many owners think they need “better bookkeeping” when what they really need is better interpretation.

Bookkeeping tells you what happened. Advisory asks whether that result is acceptable, repeatable, and worth scaling.

Here's a small example. A business owner applying for financing may know revenue, but lenders care about profit quality too. If you want a plain-English refresher on that piece, this guide on understanding net income for loan applications is useful because it shows why top-line growth alone doesn't answer the lending question.

Practical rule: If your reports don't change your decisions, you don't have advisory yet.

That's why many owners end up wanting more than compliance work. They want someone who can sit with the numbers and say, “This is the pressure point. Fix this first.”

A more strategic reporting setup helps bridge that gap. That's the idea behind how strategic accounting services turn numbers into decisions. The value isn't in fancier spreadsheets. It's in making the next move clearer.

Advisory vs Bookkeeping Accounting and CFO Services

These terms get mixed together all the time. They overlap, but they aren't the same job.

A bookkeeper records activity. An accountant organizes and reports it. An advisor helps you decide what to do with it. A fractional CFO usually goes one step further and helps lead execution.

Financial Services Role Comparison

| Role | Primary Focus | Key Question Answered |

|---|---|---|

| Bookkeeping | Recording financial history | What happened in the books? |

| Accounting | Organizing, reconciling, reporting, compliance | Are the numbers accurate and ready for reporting and tax work? |

| Financial advisory | Interpreting numbers for decisions | What should we do next? |

| Fractional CFO | Strategic leadership and financial execution | How do we plan, prioritize, and carry this out? |

Where the lines usually fall

Bookkeeping is the foundation. Bills get entered, accounts get reconciled, transactions are coded, and the records stay current. If this layer is sloppy, everything built on top of it gets shaky fast.

Accounting adds structure. Financial statements get cleaned up. The reporting becomes usable. Tax-ready records and month-end close processes start to make sense.

Advisory is where the conversation shifts from recordkeeping to judgment. Now the focus is pricing, margin, hiring, debt, cash timing, and planning around risk. This is the layer many owners are missing.

Fractional CFO is more hands-on

A fractional CFO often owns the planning cycle more directly. That may include budgeting, forecasting, lender conversations, board or partner reporting, and accountability around execution.

In real life, here's how that plays out:

- Bookkeeper. “Your accounts are updated through month-end.”

- Accountant. “Your gross profit moved down and these expenses need reclassification.”

- Advisor. “Your margin is slipping because this service line is underpriced.”

- Fractional CFO. “We're changing pricing, tightening receivables, and building a weekly cash forecast starting now.”

If your business keeps saying, “We know our numbers, but we still don't know what to do,” you're usually missing the advisory layer.

Some firms provide more than one of these functions under one roof. Others specialize in only one. If you're sorting through the difference, this breakdown of financial advisory vs consulting for business owners can help clarify where one ends and the other begins.

What You Actually Get with Financial Advisory

Most articles answer “what is financial advisory services” by circling around investments. That's not wrong. It's just incomplete for a business owner.

For small and midsize companies, the highest-value advisory work is often tied to operations. Coursera's overview of financial advisors notes that online resources usually focus on personal investing and rarely explain SMB use cases like cash-flow forecasting, KPI dashboards, and pricing decisions. That's exactly the gap most owners feel.

Deliverables that matter in the real world

A solid advisory relationship usually produces things you can use.

- Cash flow forecasting. Not a vague feeling about cash. A view of upcoming inflows, outflows, payroll pressure, debt payments, and seasonal dips.

- Profitability analysis. Which service lines, clients, jobs, or locations make money, and which ones just create busy work.

- KPI dashboards. A short list of metrics that matter to your model. Not a giant dashboard full of noise.

- Scenario planning. What happens if you hire, raise prices, buy equipment, expand space, or lose a large client.

- Budgeting tied to action. A budget that guides decisions, not one that gets ignored three weeks after it's built.

One example most owners recognize

Take a construction company. Revenue can look strong while cash stays uneven between projects. Job costing may be late. Change orders may not get tracked cleanly. The owner feels constantly short on cash even though sales are moving.

In that case, advisory work often focuses on:

- better job-cost reporting

- timing of vendor payments

- forecasted cash gaps between projects

- margin review by job type

- whether overhead has outgrown current pricing

That's not wealth management. That's operational finance.

Good advisory connects numbers to action

The best advisory isn't a thick report. It's a short list of decisions with clear financial impact.

That might mean pausing a hire, raising prices on one service line, changing payment terms, or cutting an offering that looks impressive but drags down profit. Firms like MyOfficeOps provide this kind of support through bookkeeping, financial analytics, and CFO-level advisory for SMBs that need clearer guidance on cash flow, profitability, and planning.

If growth is your focus, it also helps to pair financial planning with broader operating strategy. This article on effective small business growth strategies is a useful companion because growth only works when the financial side can support it.

Good advice should help you do one of three things. Protect cash, improve profit, or make a decision faster.

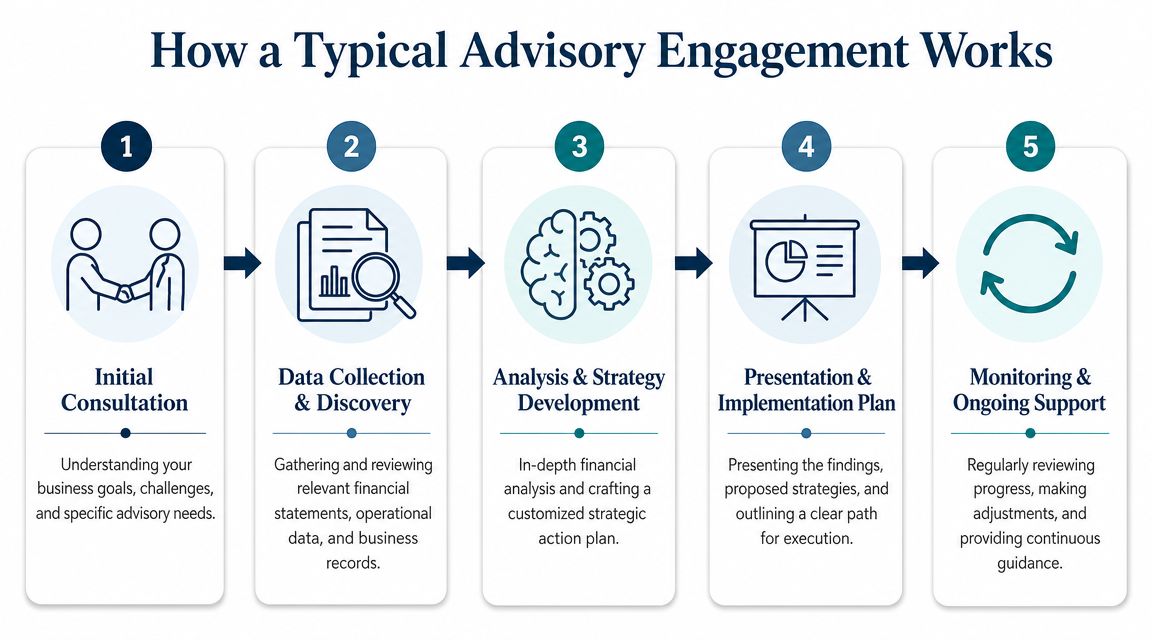

How a Typical Advisory Engagement Works

Most owners delay advisory because they think it's going to be complicated, expensive, or full of jargon.

A good process should feel pretty normal. You talk about the business. The advisor reviews the numbers. Together, you decide what needs attention first.

Step one is usually a real conversation

The first meeting should sound less like a pitch and more like a diagnosis.

The advisor asks about your goals, what feels messy, where cash gets tight, and which decisions you keep putting off. You should leave that call feeling understood, not sold to.

Then the numbers come into focus

Once there's a fit, the work usually moves through a few stages:

Discovery and data review

Financial statements, bookkeeping quality, payroll setup, debt obligations, reporting gaps, and operational pain points get reviewed.Analysis and priority setting

The advisor looks for what matters most right now. Cash flow trouble, margin erosion, weak reporting, pricing confusion, or growth without control.Plan and implementation path

You get a practical roadmap. Not fifty ideas. Usually a few priorities in the right order.Ongoing check-ins

Monthly or regular meetings keep the plan alive. Forecasts get updated. Assumptions get tested. Decisions get made with fresher information.

What the relationship should feel like

You shouldn't need a finance degree to follow the conversation.

A good advisor explains the issue in plain language, gives you trade-offs, and tells you what probably happens if you wait. Sometimes the answer is “go for it.” Sometimes it's “not yet.” Both are useful.

The best engagements are boring in a good way. Clean handoff, clear reporting, regular meetings, fewer surprises.

That's especially true for smaller businesses. You don't need a giant consulting project. You need a steady process that helps you stay ahead of cash, margin, and planning.

Finding the Right Advisor in the Philadelphia Area

If you're looking around Greater Philadelphia or West Chester, don't start with the sales pitch. Start with the fit.

Some advisors are built for personal wealth. Some are built for transactions. Some are built for operating businesses that need help making day-to-day and quarter-to-quarter decisions. Those are three different needs.

Ask better questions before you hire

A lot of business owners struggle to judge advice quality and conflicts. The label “advisor” can cover everything from planning to product sales. Wikipedia's overview of financial advisers notes that duties, licensing, and compensation can vary, which is why the real question is whether you're buying conflict-aware guidance or a sales-led product.

Ask direct questions like these:

- How do you help businesses like mine make decisions?

- What does your reporting look like, and will I understand it?

- Do you focus on cash flow, profitability, pricing, and planning, or mostly investments and products?

- How are you paid?

- If you recommend something, how do I know the recommendation fits my business and not your compensation model?

- What happens in the first ninety days?

If they can't answer those clearly, keep looking.

Pricing matters, but structure matters too

You'll hear a few common pricing approaches.

- Hourly can work if you need help on a narrow issue.

- Flat monthly fees often make sense for ongoing SMB support because they're easier to budget.

- Asset-based pricing is more common in investment-focused advisory and may be less relevant if your main problem is running an operating company better.

The best structure is the one that matches the work. If you need help with cash flow, margins, hiring decisions, and planning, you want an engagement that supports regular involvement, not random one-off calls.

Local context matters more than people think

The Philadelphia area has a wide mix of businesses. Professional services firms, medical practices, contractors, real estate operators, agencies, and family-run companies all have different rhythms. A contractor in Chester County doesn't need the same kind of guidance as a partner at a law firm in Center City.

That's where a local relationship can help. An advisor who understands the pace of the regional market, local lenders, owner-operated business culture, and the way small firms make decisions tends to be more useful than someone giving generic advice from a distance.

If your books are current but your decisions still feel harder than they should, it may be time for a real advisory conversation instead of another month of looking at the same reports.

If you want that kind of clarity, MyOfficeOps works with small and midsize businesses in West Chester, Philadelphia, and the surrounding area on bookkeeping, reporting, and CFO-level advisory. A discovery call is a simple way to see whether you need cleaner books, better reporting, or a more strategic financial partner.